●

'Adam Smith' (George Goodman) (1975). "Powers of Mind." Random House NY, p. 72.

"...They would say they were right and the market was wrong because their reasons were right.

If you're stubborn, you can lose a fortune with causality and plain logic."

●

Jane Bryant Quinn (1991). "Making the Most of Your Money." Simon & Schuster, p. 671.

"...never to buy anything whose price you can't follow in the newspapers."

●

Zweig Jason (2007). "Your Money and Your Brain." Simon & Schuster, p. 32.

"Stocks are like Weather, altering almost continuously and without warning; businesses are like climate,

changing much more gradually and predictably."

My Fragments - From My Personal Point of View

For the complete list, please see Tamari.

MF1: Fractals relate to attractors like cobblestones in roads. Added 1 January 2000.

MF7: Globalization + Computerization = Tsunamization. Added 9 October 2008.

MF8: A metaphor is a bridge from the known to the unknown. In the spirit of Ariston. Added 7 March 2009.

MF11: Collectivization and privatization are crimes against humanity. Added 24 July 2010.

MF12: A metaphor is a harpoon thrown from the known into the unknown. Added 7 August 2010.

MF18: A good metaphor is the cornerstone of a new theory. Added 20 August 2010.

MF20: Words are clouds and mathematics is the rain. Added 12 March 2012.

If you don't know the 'Game,' here is an inexpensive site to find out.

Rules

* Keep your nerves steady, since nerves are the most important part of your body when it comes to the Game.

* The Game has rules - patterns, graphs, mathematical formulas, logic, psychology and chance - but no one knows what they are for sure.

So you are free to choose your own strategy. Your personality will dictate it for you.

* Everybody has their own mix of profit-loving and risk-hating.

●

Strategic Methods:

The methods are not competitive but complementary and each method is useful in its own time.

* Cyclic Analysis provides the tools (Dow, Elliot, Fibonacci, Gann, Hurst and Speculative Cycles) to find the timing and the pricing of the market.

* Fundamental Analysis is the way to identify countries, sectors, branches, and groups to invest in.

* Security Analysis is the method to identify the stocks that are under- or overvalued (good or bad purchasing).

* Technical Analysis is the way, in the short run, to find the good or bad buy/sell price.

►If you don't believe in the predictability of the market, or have no time to manage your portfolio, buy Index Funds or Bonds.

●

I will explain here only the Speculative Cycles which I have developed. The other methods are explained in the books listed in the bibliographic list or you can use Google and Wikipedia.

'The Speculative Cycle of Stocks': 'The stock market price index (of any stock market) is deflated by the price index (CPI, inflation), the output index (GDP, economic growth) and the population index (N, population growth).'

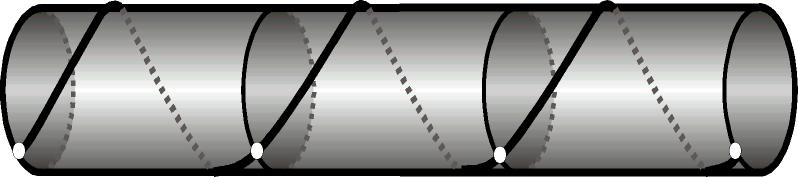

Theory - The Cylinder (Sleeve, Pipe) and the Stock Market.

The Speculative Indexes of the stock markets behave like water flowing through a cylinder (sleeve, pipe).

Assumption: The mathematical root of the speculative stock markets is the 'cylinder (sleeve, pipe) model'; see Ben Tamari (1990) "Foundations of Economics," p. 47, Figure 3.

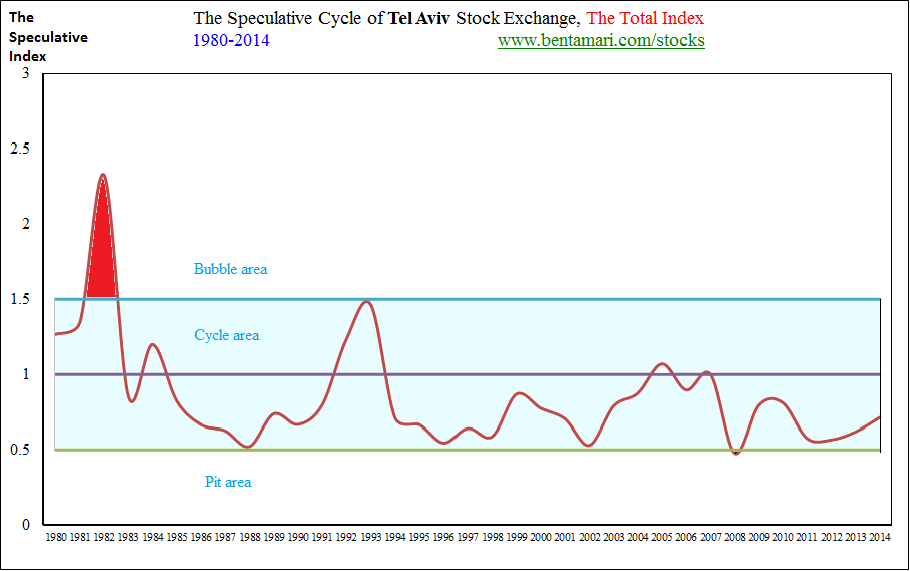

The cylinder (sleeve, pipe) ● The speculative price index of the Tel-Aviv Stock Market ● The cylinder model for the stock market.

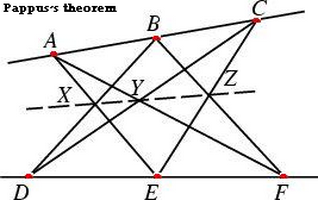

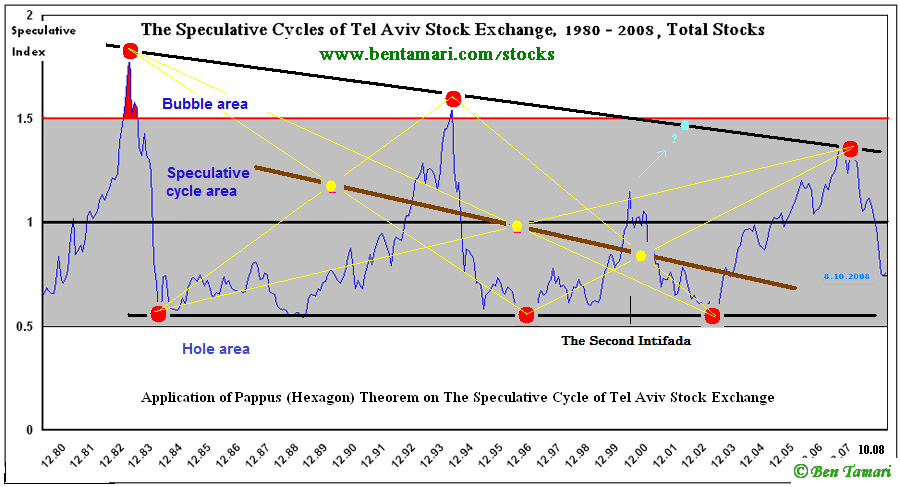

Conjecture: The mathematical basis of the stock market is Pappus's Theorem, or Pascal's Theorem (see Weisstein. "Pappus's Hexagon Theorem").

Figure 1: Application of the Pappus (Hexagon) Theorem on the Speculative Cycle of the Tel Aviv Stock Exchange.

Empiric - The Cylinder (Sleeve, Pipe) and the Stock Market

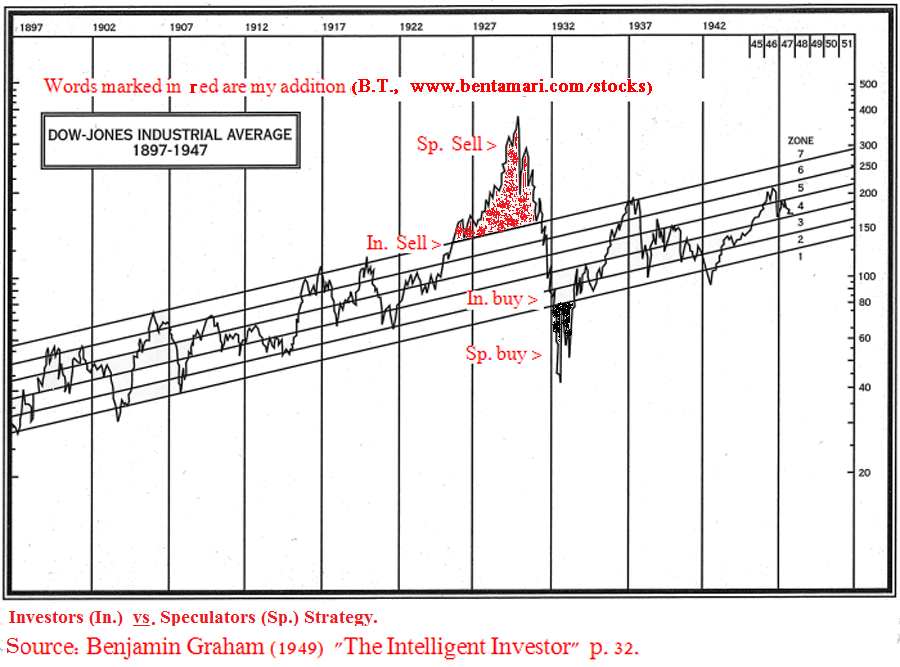

McNeel, R.W. (1921). "Beating the Stock Market." Cosimo Inc., p. 50.

"The complete cycle, occupying two or three years, has represented the transfer of stocks from the public to intelligent interests at low prices, the retransfer to the public at high prices, and the return of those stocks to the intelligent interests at low prices again. So the intelligent speculators are stronger. They have the stocks as well as the public's money, and the poor old public, the lambs, must go out and grow a new fleece." [my bold, B.T.]

Graham Benjamin (2006). "The Intelligent Investor." Revised edition, updated with new commentary by Jason Zweig. Collins, p. 189, 205.

"Since common stocks, even of investment grade, are subject to recurrent and wide fluctuations in their prices, the intelligent investor should be interested in the possibilities of profiting from these pendulum swings. There are two possible ways by which he may try to do this: the way of timing and the way of pricing. By timing we mean the endeavor to anticipate the action of the stock market - to buy or hold when the future course is deemed to be upward, to sell or refrain from buying when the course is downward. By pricing we mean the endeavor to buy stocks when they are quoted below their fair value and to sell them when they rise above such value,"

[my bold, B.T.]

"The most realistic distinction between the investor and the speculator is found in their attitude toward stock-market movements. The speculator's primary interest lies in anticipating and profiting from market fluctuations. The investor's primary interest lies in acquiring and holding suitable securities at suitable prices."

►The Speculative Cycles will assist you not to be a lamb but to detect the timing and pricing of the market within the cycle.

For example: Figure 2: Dow-Jones Industrial Average 1897-1947

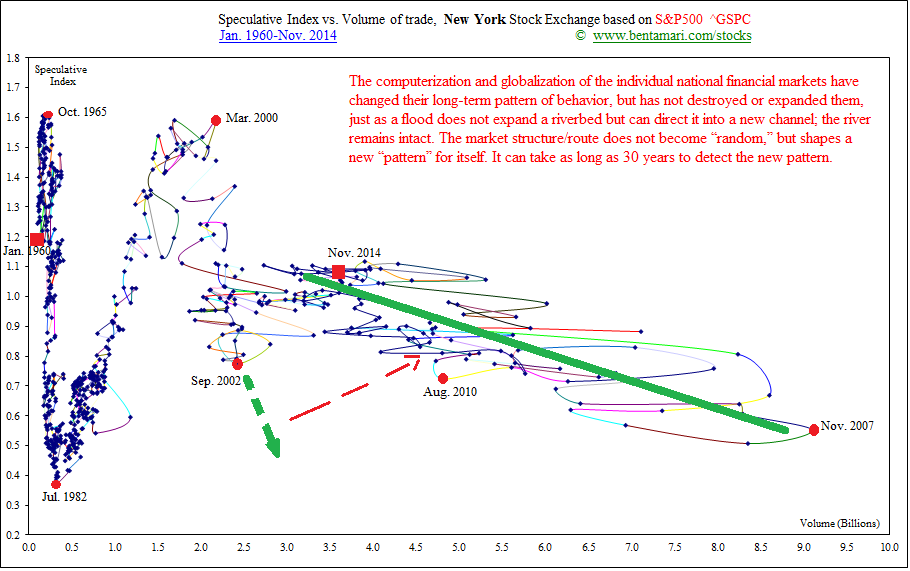

Figure 3a: The Speculative Index vs. Volume, New York Stock Exchange 1960-2012, monthly.

U Figure 3b: The Speculative Index vs. Volume, New York Stock Exchange 1960-2014, yearly.

U Figures 4, 5, 6, 7, 8: The Speculative Cycles of the London, New York, Tel Aviv, Tokyo and Toronto Stock Exchanges.

Figure 9: The Speculative Cycles of the London, New York, Tel Aviv, Tokyo and Toronto Stock Exchanges Together.

Note 1, 15 February 2007 Note on patterns

Zweig, Jason (2007). "Your Money and Your Brain." Simon & Schuster.

"The pursuit of patterns in random data is a fundamental function in our brains... ," p. 58.

Mandelbrot and Hudson (2004). "The (Mis)Behavior of Markets." Basic Books, p. 21.

"Patterns are the fool's gold of financial markets. The power of chance suffices to create spurious patterns and pseudo-cycles that, for all the world, appear predictable and bankable. But a financial market is especially prone to such statistical mirages. My mathematical models can generate charts that - purely by the operation of random processes - appear to trend and cycle. They would fool any professional "chartist." Likewise, bubbles and crashes are inherent to markets. They are the inevitable consequence of the human need to find patterns in the patternless."

Mantegna and Stanley (2000). "An Introduction to Econophysics: Correlations and Complexity in Finance." Cambridge, p. 5.

"Although it cannot be ruled out that financial markets follow chaotic dynamics, we choose to work within a paradigm that asserts price dynamics are stochastic processes. Our choice is motivated by the observation that the time evolution of an asset price depends on all the information affecting (or believed to be affecting) the investigated asset and it seems unlikely to us that all this information can be essentially described by a small number of nonlinear deterministic equations."

Following are three quotations that stand out against the ability to predict the market, since there are no patterns or equations found in stock market prices. My opinion is different, as I believe that if we have enough information about the market it will reveal the patterns or equations hidden behind it. We need at least ten cycles of reliable data. Since one cycle lasts ten years on the average, we need at least 100 years of data. So far we have only 51 years of reliable data (since 1960).

In the words of Nikolai D. Kondratieff (1950). "The Long Waves in Economic Life." In "Readings in Business Cycle Theory," American Economic Association Series, p. 34:

"Although the period embraced by the data is sufficient to decide the question of the existence of long waves, it is not enough to enable us to assert beyond doubt the cyclical character of those waves. Nevertheless we believe that the available data are sufficient to declare this cyclical character to be very probable."

In the words of Norbert Wiener (1954). "The Human Use of Human Beings." Da Capo Press, p. 21.

"Messages are themselves a form of pattern and organization."

In the words of Sunny Y. Auyang (1998). "Foundations of Complex-System Theories in Economics, Evolutionary Biology, and Statistical Physics." Cambridge UP, p. 2.

"One cannot see the patterns of a mural with his nose on the wall; he must step back."

Note 2, 15 January 2008 Note on "predicting the unpredictable."

Zweig, Jason (2007). "Your Money and Your Brain." Simon & Schuster. p. 56, 58, 65, respectively.

"No one can predict the unpredictable."

"The pursuit of patterns in random data is a fundamental function in our brains... ."

"Just as nature abhors a vacuum, people hate randomness...I call this human tendency 'the prediction addiction.'"

...but he declared that 'predictable phenomena' are 'unpredictable.'

●

Wislawa Szymborska (1996). "Ending and Beginning." Translated by Deena Land (11 August 2010).

"Maybe All This

Without intervention?

The changes are self occurring?

According to plan?

The graph needle slowly draws

The foreseen zigzags?"

●

Take a look at these two pictures: the first is the Jordan River and the second is "Speculative Stock Index vs. Volume Trade"; from the point of view of predictability, what is the difference?

The computerization and globalization of the individual national financial markets have changed their long-term pattern of behavior, but has not destroyed or expanded them, just as a flood does not expand a riverbed but can direct it into a new channel; the river remains intact. The market structure/route does not become “random,” but shapes a new “pattern” for itself. It can take as long as 30 years to detect the new pattern.

N Meanderiness of a river. Added 22 December 2014.

http://blog.matthen.com/post/85019675571/the-meanderiness-of-a-river-its-st-lum-number-is

http://i.imgur.com/Uak4YU3.gif

Note 3, 28 February 2014 Note on "cylinder theory"

Carlo Maria Flumiani (1961, reprinted in 2013 by Alanpuri Trading). "The Cylinder Theory." The Institute for Economic and Financial Research.

"POSITION OF THE STOCK IN THE CYLINDER

...to determine the position of a single security or of a group of securities or of the whole market measured by the averages within the cylinder," [my bold, B.T.] p. 44.

"THE CYLINDER THEORY

The Cylinder Theory is nothing else but the representation of the Law of

Conflict and Change, the cardinal law of man and of his history. Having

recognized that:

... Escape is the dominant drive prompting men to action

... Escape terminates in change

... All changes are preceded by a condition of conflict

... The terms of the conflict, of all conflicts, are easily

known.

The Cylinder Theory maintains that from an analysis of the conflict one

can anticipate the nature and the course of the change," p. 19.

Ben Tamari (2000).

{kind=link}